Defining the cash-flow problem

Many working households in Mexico face predictable monthly shortfalls driven by fixed expenses and occasional spikes — medical bills, vehicle repairs, or school fees. The immediate need is not just cash but a disciplined, affordable way to cover gaps without creating worse financial strain. A practical option appearing in urban centers, especially Mexico City since 2020, is short-term online credit; providers now compete on speed and clarity. For a straightforward entry point to these options, consider didi prestamos which positions itself as a fast, standardized alternative for urgent liquidity.

Why typical quick-loan approaches fail

Quick loans often promise speed while masking costs. Borrowers focus on immediate availability and overlook the interest rate, repayment term, and the loan’s impact on their credit score. The result is a short-term fix that raises monthly obligations later. Lenders without clear underwriting or transparent APR create unpredictability for household budgets — and that unpredictability is the real problem, not the loan itself.

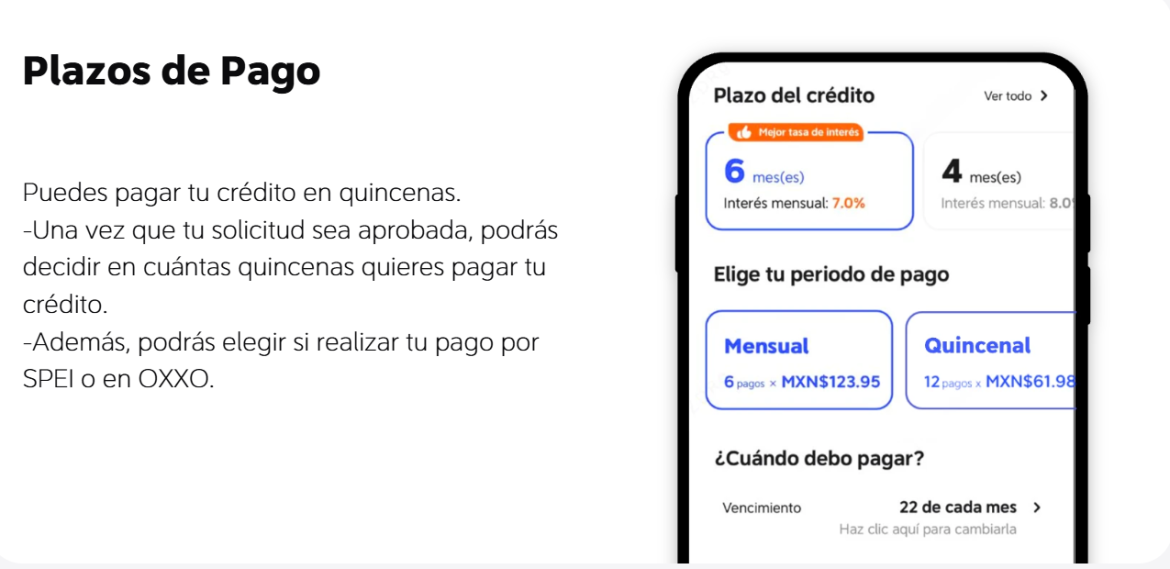

How DiDi Finanzas addresses the problem

DiDi Finanzas reframes online short-term loans into a budget tool by standardizing disclosures and streamlining repayment schedules. That approach reduces ambiguity around fees, makes cash-flow projections reliable, and integrates digital account statements that track scheduled debits. For users seeking simple, fast credit, the model aligns immediate funding with predictable outflows — the kind of system that turns an emergency loan into a controlled cash management tactic. For those comparing providers, also review offerings labeled prestamos en linea rapidos to verify processing times and fee transparency.

Practical implementation steps

Adopt this four-step routine when evaluating fast online loans: assess net monthly cash inflow against essential expenses; calculate the exact gap; match loan size to the gap plus a 10–15% buffer for fees; and choose a product with clear repayment dates. Start with a conservative borrowed amount and prioritize lenders that provide digital amortization schedules. These steps make a high-speed loan a tactical resource instead of a recurring dependency.

Common mistakes and sensible alternatives

Borrowers commonly take larger loans than needed, chase longer terms to lower monthly payments, or ignore documentation — triggers for higher total cost. Alternatives include short-term employer advances, community credit unions in Mexico City, or staggered payments negotiated with service providers. If a particular product lacks clear APR disclosure or a transparent underwriting policy, walk away — that’s often an indicator of downstream surprises. — It’s a small precaution that prevents larger budget shocks.

Evaluating options: three metrics that matter

When comparing quick-credit products, use these three golden rules: 1) Total cost visibility — ensure all fees and APR are disclosed up front; 2) Cash-flow fit — verify the repayment term matches your budget cycle so monthly obligations remain steady; 3) Service reliability — confirm digital statements and customer support in your time zone, especially relevant for urban Mexican markets where turnaround matters. These metrics focus selection on measurable outcomes rather than marketing claims.

Conclusion and actionable takeaways

Adopting a problem-driven view reframes fast online loans from risky shortcuts into tactical tools for monthly budgeting. Assess costs, align terms to your cash-cycle, and prefer lenders that deliver clear amortization and timely support. When these conditions are met, a quick loan can stabilize a month without becoming a recurring liability. For many urban households — including those in Mexico City adapting since 2020 — that stability is precisely the value DiDi Finanzas aims to deliver. DiDi Finanzas.

–